Detailed Overview of Economic Events and Corporate Reports for Wednesday, December 3, 2025: Global PMIs, Inflation Data, Major Company Reports, "Russia Calls!" Forum, and Key Indicators for Investors.

Wednesday promises a rich economic agenda for the markets. In Asia, investors are keeping an eye on key indicators: Australia will release GDP data and the services PMI, while Japan, China, and India will publish their November PMIs. In Europe, the focus will be on the services PMIs for Germany, the Eurozone, and the UK, along with ECB President Christine Lagarde's speech at public hearings in Strasbourg. In the US, attention will be directed toward employment statistics (ADP) and activity in the services sector (ISM and S&P indices), as well as weekly oil inventory reports (EIA). Concurrently, significant events are taking place, including French President Emmanuel Macron's official visit to China and the second day of the "Russia Calls!" investment forum. Investors should link macroeconomic results with market dynamics: inflation and PMI ↔ yields, commodities, risk appetite.

Macroeconomic Calendar (Moscow Time)

- 01:00 — Australia: Services PMI (November).

- 03:30 — Australia: GDP (Q3 2025, YoY).

- 03:30 — Japan: Services PMI (November).

- 04:45 — China (Caixin): Services PMI (November).

- 08:00 — India: Services PMI (November).

- 09:00 — Russia: Services PMI (November).

- 10:00 — Turkey: Consumer Inflation CPI (November).

- 10:30 — Switzerland: Consumer Inflation CPI (November).

- 11:55 — Germany: Services PMI (November).

- 12:00 — Eurozone: Services PMI (November).

- 12:00 — Russia: Central Bank announces volumes of currency market operations.

- 12:30 — UK: Services PMI (November).

- 13:00 — Eurozone: Producer Price Index PPI (October).

- 16:00 — Brazil: Services PMI (November).

- 16:15 — USA: ADP Employment Estimate in the Non-Farm Sector (November).

- 16:30 — Europe: Speech by ECB President C. Lagarde (EU Parliament hearings).

- 17:15 — USA: Industrial Production Index (September).

- 17:30 — Canada: Services PMI (October).

- 17:45 — USA: S&P Global Services PMI (October).

- 18:00 — USA: ISM Services PMI (November).

- 18:30 — Europe: Lagarde's repeat speech (financial risks, EU hearings).

- 18:30 — USA: EIA Oil Inventory Report (weekly).

- 19:00 — Russia: Consumer Inflation CPI (November).

Asia

- Australia: GDP Data (Q3 2025) and Services PMI (November). A recent cut in the RBA's key rate heightens expectations of moderate economic growth. Moderate GDP and stabilization in PMI could strengthen the AUD and support Australian assets.

- Japan and China: November Services PMI indices (03:30 and 04:45 Moscow time). These will provide signals about the recovery in domestic demand. A slowdown in PMI in both countries may dampen risk sentiment in the markets.

- India: Services PMI (08:00 Moscow time). The index often leads economic growth: a strong result will emphasize the strength of the Indian economy amid GDP growth.

Force majeure: French President Emmanuel Macron's state visit continues in Beijing, highlighting China's geo-economic significance. No market impact is expected; however, attention to the negotiations may increase volatility in Asia-Pacific stock indices.

Europe

- Eurozone, Germany, UK: Services PMIs for November (11:55–12:30 Moscow time). Stabilization is expected after previous declines: a weak PMI will slow euro equities, while improvement will support risk appetite.

- Switzerland, Turkey, Eurozone: Inflation data. At 10:30 – Switzerland CPI (November), at 10:00 – Turkey CPI (November), and at 13:00 – Eurozone PPI (October). Rising prices in Europe may increase pressure on the ECB, pushing currencies to strengthen against the dollar.

- ECB (Lagarde): Speeches (16:30 and 18:30 Moscow time). The head of the ECB, speaking before the EU Parliament, may provide a boost to the euro and bonds: tough rhetoric will strengthen the EUR, while calls for easing will weaken it.

Russia

- "Russia Calls!" Forum: second day of the VTB forum. Discussions on new investments in sectors continue, with potential announcements from state companies and regulators anticipated.

- Bank of Russia: at 12:00, will announce volumes of currency purchases/sales. A small currency deficit will support the ruble, while a surplus will weaken it. The volumes affect market liquidity.

- Data from Russia: Services PMI (09:00 Moscow time) and Consumer Inflation CPI (19:00 Moscow time). A slowdown in PMI reflects stagnation in domestic spending; accelerated CPI will increase pressure on rates and the ruble.

Together, these factors create a backdrop for the Russian market: rising inflation and oil volatility may hold the ruble back, while the outcomes of the forum will set investors' portfolio mood.

USA and North America

- USA: The ADP employment report (16:15 Moscow time) will show hiring dynamics outside the agricultural sector. Strong data will accelerate labor market growth and may increase treasury yields; weak data will weaken the dollar. Following that, at night (18:00 Moscow time) – the ISM Services Index (November), and at 17:45 – S&P Global Services PMI. A coincidence of PMI and ISM indices will indicate trends in the services sector, where jobs are created: an acceleration is favorable for stocks, while a slowdown is not.

- Canada: Services PMI (17:30 Moscow time). Stability in Canadian PMI will support the Bank of Canada's policy and CAD; an unexpected decline will weaken it.

- Corporate Reporting (USA): Major players are reporting results. Salesforce (CRM) – after market close (press release and teleconference at 2:00 Moscow time), Macy’s (M) – before opening (8:00 ET), PVH (PVH) – after close, Five Below (FIVE), Torrid (CURV), Guidewire (GWRE), Sprinklr (CXM), Inotiv (NOTV) – also reporting. These may cause additional volatility: successful reports will boost demand for sector stocks, while disappointment will weaken it.

- Chinese Companies: Waterdrop (WDH) and Yuanbao (YB) – reports for Q3 (before market opens). As online insurers, they will give sensitivity to internal demand in the PRC; publication before opening will allow for prior adjustments in evaluations.

Commodities and Currencies

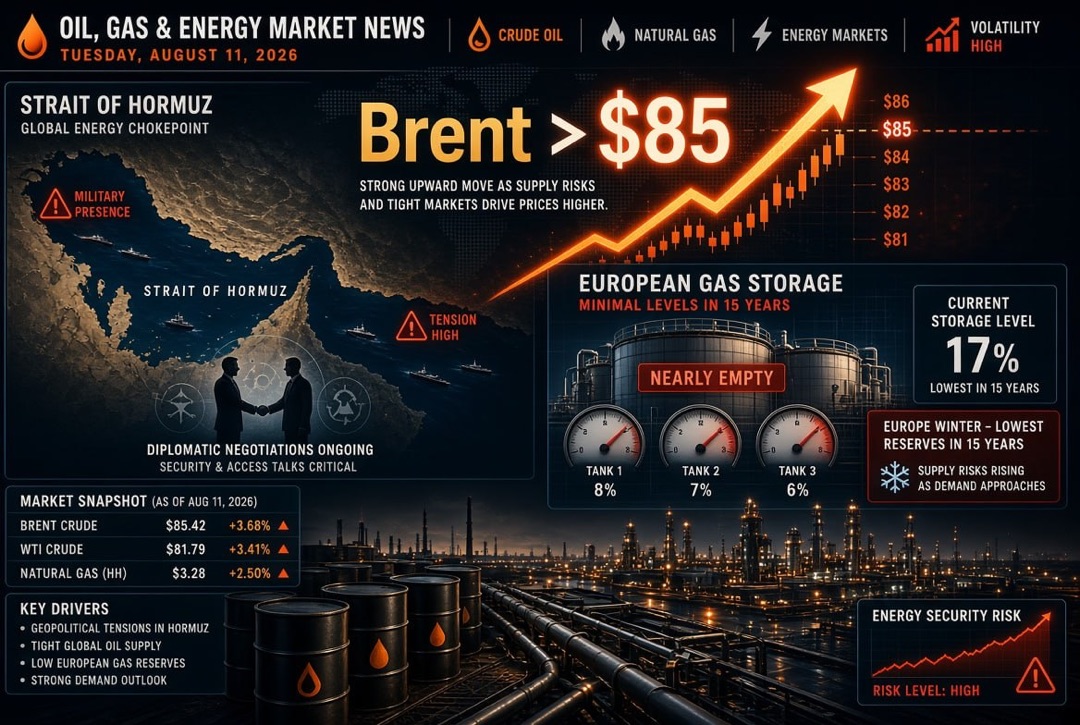

- Oil: EIA report (18:30 Moscow time). A decrease in commercial inventories is expected after seasonal demand: a more significant drawdown will support Brent/WTI prices, while an increase will exert pressure.

- Commodity Prices: The overall background remains stable – metals are up, oil around $75. A strengthening dollar is moderately slowing commodities. Investors will be monitoring OPEC+ actions and demand dynamics.

Corporate Reporting

- USA, Retail and Technology Sectors: Salesforce (NYSE: CRM) – Q3 FY2026 after the close; Macy’s (NYSE: M) – Q3 2025 before the opening; Five Below (NASDAQ: FIVE) – Q3 fiscal 2025 after the close; Torrid Holdings (NYSE: CURV) – Q3 after the close; PVH Corp (NYSE: PVH) – Q3 after the close. Retail chains and technology services are in focus after the holiday season.

- USA, Other Sectors: Guidewire Software (NYSE: GWRE) – Q1 FY2026 after the close (Finance/Insurance), Sprinklr (NYSE: CXM) – Q3 FY2026 before the opening (Social Media, CRM), Inotiv (NASDAQ: NOTV) – Q4 FY2025 after the close (Scientific Services).

- China: Waterdrop Inc. (NYSE: WDH) – Q3 2025 before the opening (online insurance); Yuanbao Inc. (NASDAQ: YB) – Q3 2025 before the opening (online insurance). Their performance reflects demand for insurance services and the investment climate in China.

What Investors Should Pay Attention To

- PMI and ADP data in the US — will indicate the strength of consumer and business demand: growth will boost stock indices, while weak results will signal a "turn" in the macro cycle.

- ECB President Lagarde's speech — her tone will lay the groundwork for ECB rate expectations: tough rhetoric will support the euro and euro bonds.

- Oil inventories (EIA) — will become a catalyst for oil prices: the difference from forecasts will set the mood for energy stocks.

- Quarterly corporate reports (Salesforce, Macy’s, etc.) — they will determine the dynamics of the stock sector: breakthrough results may heat the race for indices, while weak results may cool the market.

- Russian factor — results from **forums and inflation**: it is important for investors to monitor the geopolitical backdrop and price growth indicators that affect the ruble and Moscow Exchange stocks.