Analysis of Economic Events and Corporate Reports for Thursday, December 4, 2025: Putin's Visit to India, Macron's Visit to China, Brazil's GDP, US Unemployment Claims, Canada’s PMI, and Global Company Reports.

Thursday promises a diverse agenda for investors in global markets. World stock indices—from the American S&P 500 and the Japanese Nikkei 225 to the European Euro Stoxx 50 and the Russian MOEX index—are hovering near recent highs amid signs of slowing inflation and soft signals from central banks. Attention now shifts to fresh economic events and corporate reports: high-level diplomatic visits in Asia, key macroeconomic data (Brazil's GDP, US employment statistics, Canada’s PMI), and financial results from several major companies. Investors will need to reconcile these factors with market dynamics: strong growth and employment figures will support risk appetite, while negative surprises may heighten volatility.

Macroeconomic Calendar (MSK)

- 00:30 — US: Weekly API Report on Crude Oil Inventories.

- 13:00 — Eurozone: Retail Sales (October).

- 15:00 — Brazil: GDP for Q3 2025.

- 16:30 — US: Initial Claims for Unemployment Benefits (week).

- 18:00 — Canada: Ivey PMI Business Activity Index (November).

Asia

- Asian markets will not receive significant new statistics on this day, so regional indices (such as Japan's Nikkei 225 and China's Shanghai Composite) will look to external signals. Investor sentiment in Asia heavily depends on global trends and news, and the lack of domestic data makes them more sensitive to events in the US and Europe.

- Force majeure: The state visit of French President Emmanuel Macron to China continues (December 3-5). Meetings in Beijing aim to strengthen EU-China trade and economic cooperation. While breakthrough agreements are not expected, the fact of dialogue between these two major economies emphasizes China's geo-economic significance. For financial markets in the Asia-Pacific region, the direct impact of these negotiations will be neutral; however, any statements following the visit may short-term heighten volatility in specific sectors (such as aviation or technology, if relevant deals are discussed).

Europe

- The Eurozone will release data on retail sales for October (13:00 MSK). The reading is expected to remain close to neutral, following a slight decline in September. The state of consumer demand is an important indicator for Europe’s economic health: an unexpected decline in sales would heighten concerns about an economic slowdown, while growth above expectations would support European stocks and the euro.

- European markets will generally spend the day without major internal disruptions, focusing predominantly on external factors. Corporate reports from specific companies are in the spotlight: for instance, German metallurgical company Aurubis will publish financial results, while British retailer Frasers Group will report on operational successes. These updates could move their respective stocks, but the overall impact on the broader European market will likely be limited. The Euro Stoxx 50 index maintains relatively stable dynamics, reacting primarily to general signals related to the global economy and monetary policy.

Russia

- Russian President Vladimir Putin begins an official visit to India (December 4-5). Talks with the Indian leadership are focused on deepening trade ties, energy cooperation (including potential new agreements for oil and gas supplies), and joint investment projects. The signing of major contracts—such as those in the defense industry or raw resources—could strengthen the positions of Russian corporations in these sectors over time. However, the short-term impact of this visit on the Russian stock market is expected to be limited, serving more as a strategic factor rather than a direct market driver.

- No new macro data is expected in the Russian market on Thursday, following the publication of November inflation the day before. The corporate earnings season on the Moscow Exchange is nearing its end—most major issuers have already revealed results for the third quarter. In the absence of fresh internal triggers, investors will look at external factors: oil prices, global market movements, and currency factors. The Russian ruble remains within a relatively stable range around 78 per dollar, receiving support from export revenues and the Ministry of Finance's currency interventions.

USA and America

- In the US, the focus is on the labor market. Weekly initial claims for unemployment benefits (16:30 MSK) will serve as a leading indicator ahead of the key employment report (Nonfarm Payrolls) on Friday. If the number of new claims decreases significantly, this will confirm the resilience of the labor market, which could bolster expectations for a tighter Fed policy (putting pressure on bonds and supporting the dollar). Conversely, a rise in claims would signal a cooling economy and weaken arguments for rate hikes, which would be perceived positively by stock indices.

- In Latin America, the highlight is Brazil’s GDP for Q3. Continuation of moderate growth in the region's largest economy is expected, driven by resilient domestic demand and raw material exports. Strong data would bolster investor confidence in emerging markets and support Brazil's Bovespa index, while weak GDP could lead to a reallocation of capital toward safer assets. Additionally, at 18:00 MSK, the Ivey PMI Business Activity Index in Canada will be released: this figure will reflect the state of Canadian business in November. A PMI rise above 50 points will indicate economic expansion and may strengthen the Canadian dollar, while a decline in the index will intensify discussions on possible stimulus from the Bank of Canada.

- Corporate earnings reports (US and Canada): A number of major companies will report financial results, which may lead to increased volatility in certain stocks. Before US exchanges open, quarterly reports from leading Canadian banks (Toronto-Dominion Bank, Bank of Montreal, CIBC) and one of America’s largest retailers, Kroger, will be released. After the market close, reports will follow from technology giant Hewlett Packard Enterprise, cosmetics store chain Ulta Beauty, discount retailer Dollar General, e-document management software developer DocuSign, and others. If the results exceed expectations, the respective stocks may surge, setting a positive tone for the sector overall (from financials to consumer goods). Conversely, disappointing results could trigger sell-offs in specific segments and hinder the growth of the S&P 500 and NASDAQ indices.

Commodities and Currencies

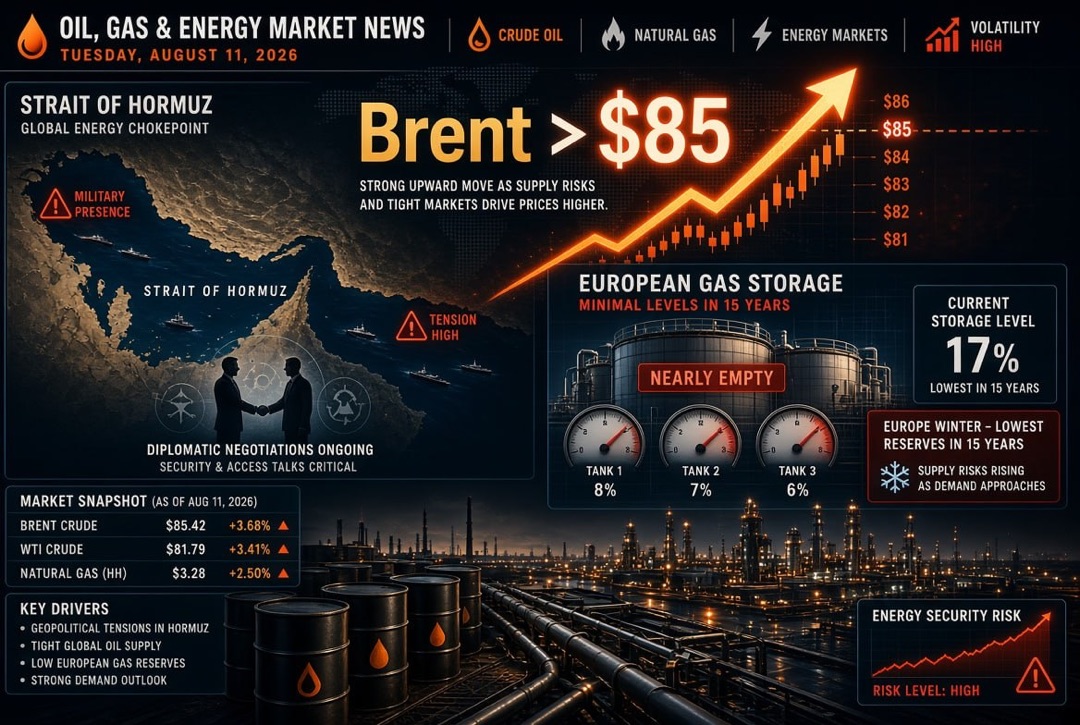

- The oil market is closely monitoring data from the American Petroleum Institute (API) on crude oil inventories in the US, released overnight. Preliminary estimates indicate a decline in commercial inventories amid increased fuel consumption during the holiday transport period. If the actual drop in inventories is greater than expected, Brent and WTI prices will receive an additional upward impulse. Conversely, an increase in inventories or a less substantial reduction could pause the price rally. Additionally, traders are evaluating the outcomes of the recent OPEC+ meeting and signals regarding future production, which affect mid-term expectations in the oil market.

- Commodity markets, in general, are maintaining a relative equilibrium. Industrial metals are trading slightly higher, supported by recovering demand in China, while precious metals are consolidating after recent gains. The foreign exchange market reflects a softening rhetoric from the Fed: the US dollar index is declining to its lowest points in recent months, allowing currencies of emerging markets and commodity currencies (like the Canadian dollar) to feel more secure. The euro and pound remain stable against the dollar, supported by local data. At the same time, the Russian ruble remains relatively stable, balancing the influence of recent increases in oil prices with internal factors. Investors are carefully observing trends in the currency market to timely assess risks for their international portfolios.

Investor Focus

- US Labor Market Data: The figure for new unemployment claims will provide an early signal of economic conditions before the official employment report. A sharp decrease in claims will heighten expectations for economic growth and could stir bond yields, while an increase in claims will bolster arguments for a quick easing of Fed policy.

- Quarterly Reports from Market Leaders: Financial results from companies like Kroger, Dollar General, HPE, and major Canadian banks reflect the health of several sectors—from consumer demand to the banking system. Investors should compare the figures released with forecasts: exceeding expectations could drive stocks in these sectors higher, while weak reports could prompt declines and a reassessment of industry outlooks.

- Oil Market Situation: The dynamics of oil prices following the API inventories report will provide cues for the oil and gas sector. A significant reduction in inventories and subsequent oil price increases will boost sentiment in the energy segment and support export-oriented markets (including Russia); meanwhile, an unexpected rise in inventories could temporarily weaken oil futures and the associated company stocks.