Analytical Review of Key Economic Events and Corporate Reports for Sunday, December 7, 2025. Macroeconomic Statistics from China and Japan, Impact of OPEC+ Decisions, and Investor Expectations Ahead of a New Trading Week.

Sunday, December 7, 2025, promises to be a relatively quiet day for global markets. Major U.S. and European exchanges are closed for the weekend, and no new corporate reports are expected on this day. Investor focus will be on important macroeconomic publications from Asia, which may shed light on the state of the global economy as the year comes to a close. These developments could influence trader sentiment ahead of market openings on Monday, thus requiring attention from investors in the CIS region, even in the absence of activity on Western exchanges.

USA (S&P 500 Index)

- The American markets will be closed on Sunday, and there are no significant economic releases or corporate reports from S&P 500 companies scheduled for December 7. U.S. investors are still digesting the latest labor market statistics published on Friday: the Non-Farm Payrolls report for November indicated a further slowdown in hiring and a persistently high unemployment rate. The lack of new data on this day leads the focus to upcoming events of the week—particularly, market participants are assessing how recent macroeconomic trends will impact the Federal Reserve's decisions at the upcoming December meeting.

Europe (Euro Stoxx 50 Index)

- Similarly, in Europe, no significant economic events are anticipated on December 7—regional markets are taking a break, and there are no corporate earnings releases from companies included in leading indices such as the Euro Stoxx 50 for Sunday. Following the conclusion of the trading week, European investors are pausing and preparing for the release of a new set of statistics early next week. Key data expected includes Germany's industrial production figures and trade activity in the Eurozone, set to be released on Monday. Additionally, there's an important event looming for Europe: a meeting of the European Central Bank scheduled for mid-December. Thus, the lack of news on Sunday gives EU markets time to regroup ahead of a potentially eventful week.

China: Trade Statistics for November

- China is set to publish external trade data for November, which will attract market attention even on a weekend. Economists forecast that exports from China are poised to return to growth, around +3-4% year-on-year after an unexpected decline of 1.1% in October. This potential improvement can be attributed to the trade truce reached at the end of October between the U.S. and China, which eased some mutual tariffs. China's imports are also likely to have accelerated (expected at around +2-3% year-on-year compared to a weak +1.0% month-on-month growth last month), despite ongoing internal demand contraction. Official Chinese customs statistics will be released on the morning of December 8, but market participants are assessing the potential impact of these figures on Sunday: strengthening Chinese exports and imports may signify a stabilization of the world's second-largest economy and bolster optimism in global commodity and raw material markets.

Japan: GDP for Q3 2025 (Final Estimate)

- In Japan, the final assessment of GDP for the third quarter of 2025 will be issued late on December 8. According to preliminary data, Japan's economy contracted by 0.4% quarter-on-quarter (which corresponds to a –1.8% annual rate)—marking the first GDP decline in the past six quarters. Revised figures may slightly differ from the initial estimate: updated data on corporate investments (capital expenditures rose by 2.9% year-on-year in Q3 but fell by 1.4% quarter-on-quarter) indicate some weakening in domestic demand. Nevertheless, the results for the third quarter will reaffirm the external pressures (declines in exports due to U.S. tariffs) alongside a relative resilience in domestic consumption. Investors will be closely monitoring this release: although Japanese markets are closed on Sunday, information regarding the real condition of the economy could potentially impact the Nikkei 225 index and the yen's exchange rate when Tokyo's trading commences on Monday.

Oil Market and OPEC+ Decision

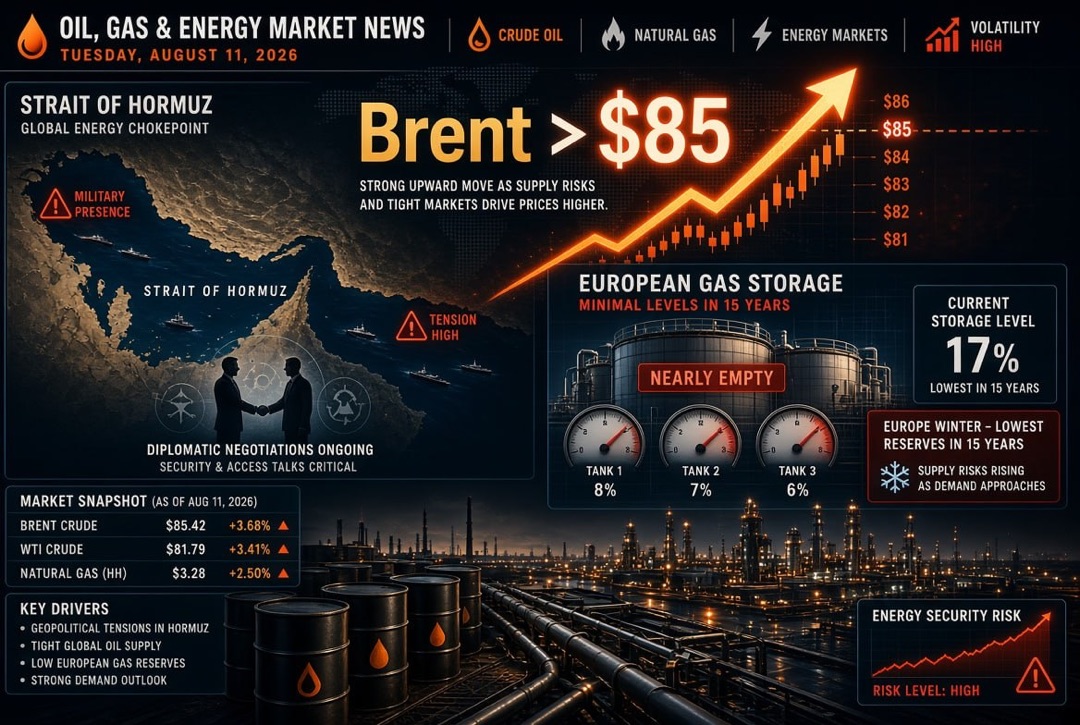

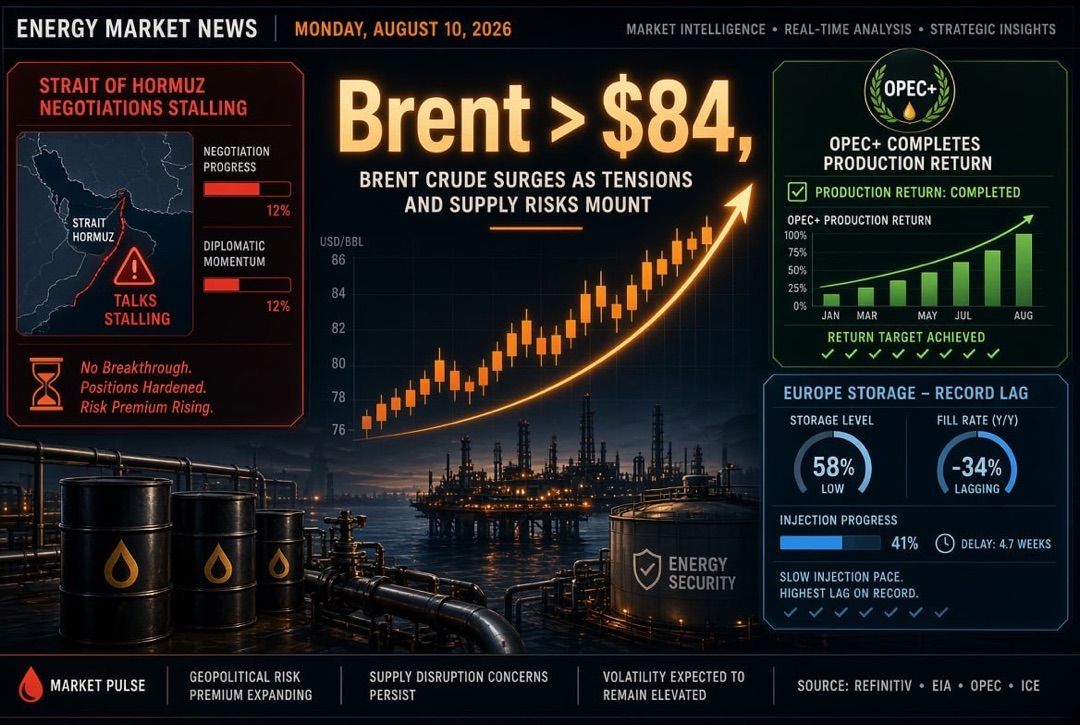

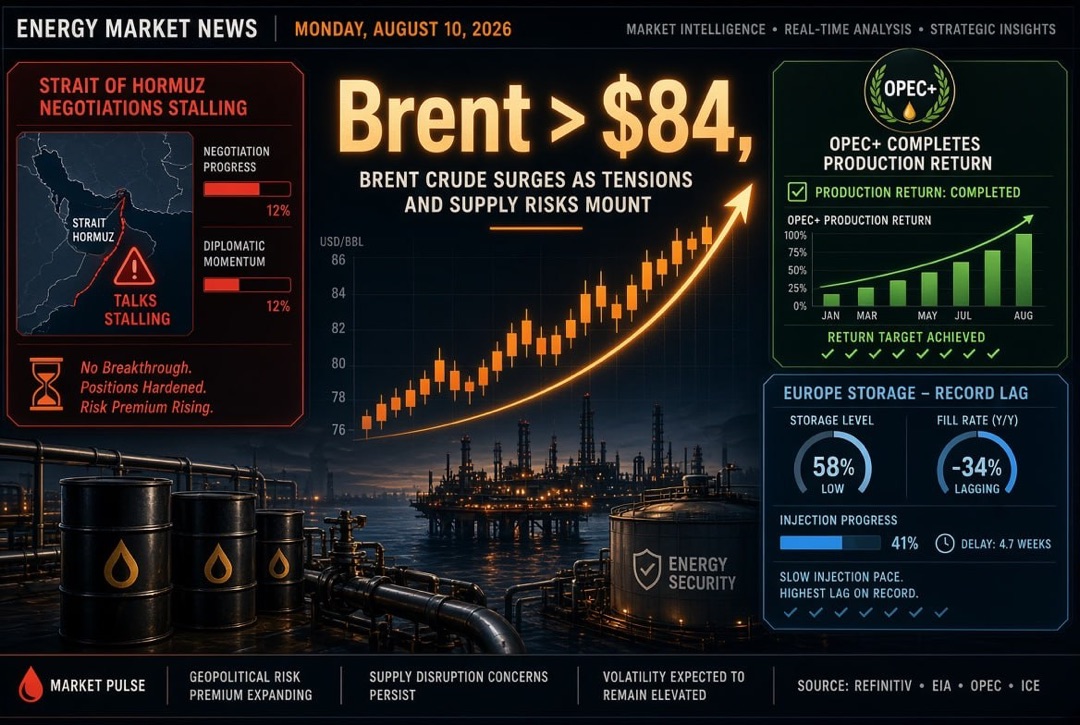

- In commodity markets, investors are evaluating the implications of recent OPEC+ decisions, even though the official meeting occurred on Saturday. The alliance countries agreed to slightly increase the oil production target in December (by 137,000 barrels per day), followed by a pause to refrain from raising quotas during the first quarter of 2026 due to the risk of oversupply. These measures were anticipated and already factored into prices: Brent crude oil prices remain around $64-65 per barrel after dipping to a five-month low of approximately $60 at the end of October. The stabilization of oil prices is favorable for commodity companies and exporting economies. In the absence of trading in exchanges on Sunday, oil price volatility remains low; however, any unexpected statements from OPEC+ participants or geopolitical news could cause fluctuations in the energy market ahead of the new week.

Russia (MOEX Index)

- For the Russian market, December 7 is a holiday: trading on the Moscow Exchange will not take place, and there are no financial reports scheduled for major companies (included in the MOEX index) on this date. Nonetheless, it is crucial for Russian investors to monitor the external backdrop forming on Sunday. Notably, oil price dynamics following the OPEC+ decision and fresh data out of China will serve as indicators capable of influencing market sentiment in Russia. Given that China plays a key role as a consumer of raw materials, a potential rise in Chinese exports and imports will likely support the prices of industrial metals and oil, positively impacting the shares of commodity companies in Russia. Thus, despite the local agenda's quietness, external factors on this day will set the stage for movements in the Russian ruble and stock indices when trading resumes on Monday.

Overall, the current Sunday is not abundant in events; however, several Asian statistical releases and recent decisions in the commodity market create an informational background significant for global investors. It is recommended to pay attention to the results of China's foreign trade statistics and the revised Japanese GDP—these indicators will aid in assessing the state of the global economy ahead of a new trading week. Any unexpectedly strong (or weak) data could influence expectations regarding central bank actions and appetite for risk. Finally, the focus will soon turn to the first of the important meetings of the upcoming week: early Monday morning, there will be a meeting of the Reserve Bank of Australia (RBA), the outcome of which will set the tone for trading in the Asia-Pacific region and serve as a benchmark for subsequent regulatory actions.